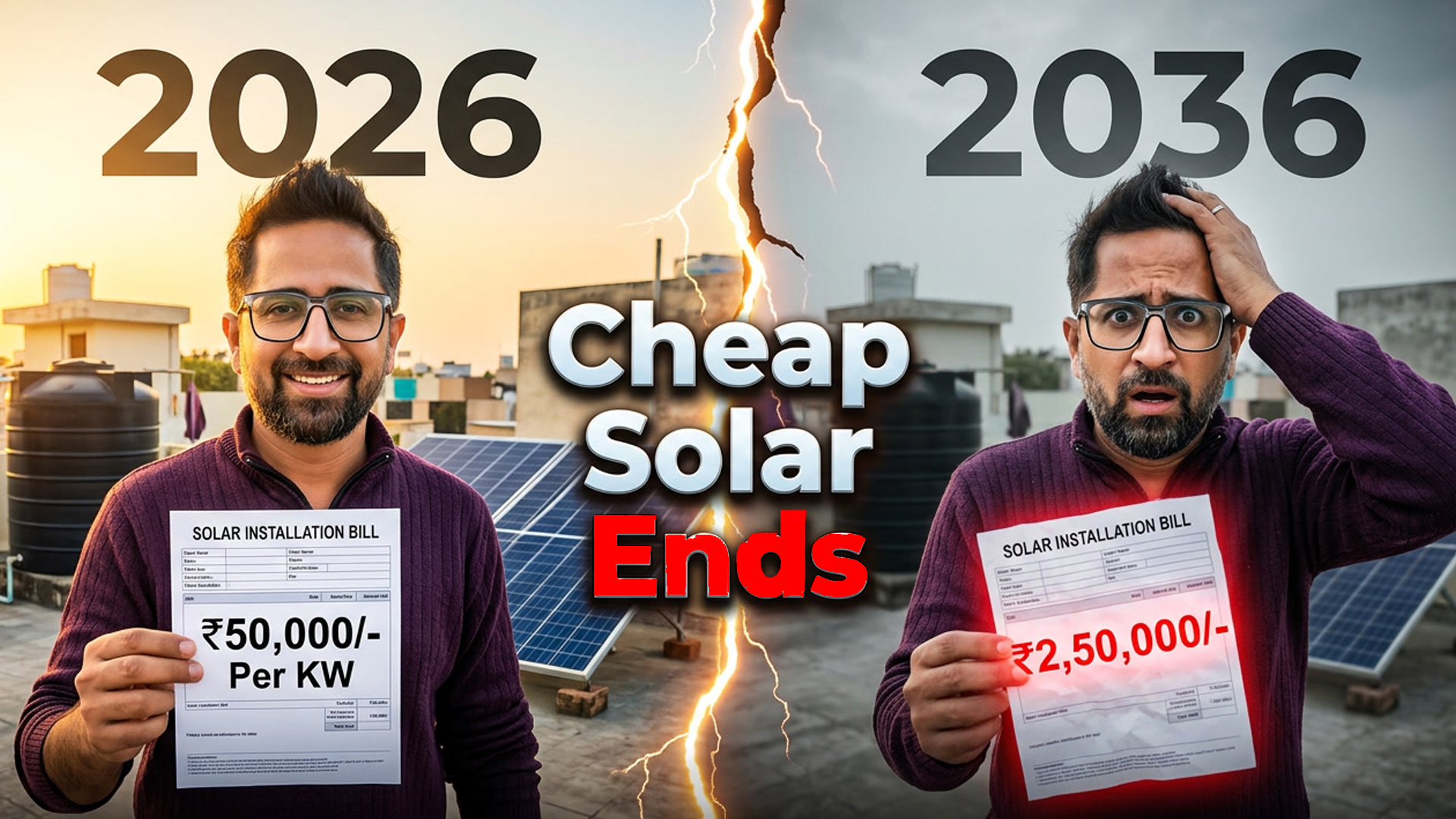

Introduction

Agar aapne 2021 ya 2022 mein rooftop solar lagaya hoga, toh aapne ek genuinely golden window pakda tha. Chinese modules globally flood kar rahe the, prices historically low thi, net metering generous tha, aur payback period 4–5 saal thi.

Woh window close ho rahi hai. Slowly, but definitely.

Yeh post 4 structural reasons cover karti hai — policy data, ministry circulars, aur international precedents ke saath backed — jo India mein rooftop solar ki cost ko next 3–7 saal mein materially badlenge.

Reason 1: DCR & ALMM Mandate — Made in India ka Cost

What changed: India’s government has made Domestic Content Requirement (DCR) the foundation of its solar policy. Under PM Surya Ghar: Muft Bijli Yojana, subsidized residential systems must use modules made from domestically manufactured cells — and those modules must appear on the ALMM (Approved List of Models and Manufacturers).

More significantly, MNRE’s March 2026 FAQ extended this beyond subsidized homes: net metering and open access projects commissioned on or after 1 June 2026 must source modules from ALMM List-I and cells from ALMM List-II.

What it costs:

- DCR modules carry a premium of approximately ₹12 per watt over non-DCR alternatives (Mercom India)

- For a 3kW residential system: roughly ₹36,000 in additional cost — just from the module premium

- Utility-scale analysis shows DCR mono-PERC projects cost 24% more than non-DCR equivalents; DCR TOPCon projects cost 37–38% more than Chinese module alternatives

Why the government is doing this: This is industrial policy wearing an energy-policy mask. The PLI program helped install approximately 11 GW of module manufacturing capacity and 5 GW of cell manufacturing capacity by 2025. India crossed 100 GW of ALMM-listed module manufacturing capacity in August 2025. The state is willing to make solar costlier for end users in the short run if it builds domestic supply chains and reduces import dependence.

The framing to remember: this is not cheap solar vs no solar. It is cheap solar vs sovereign solar. And sovereign solar is winning.

Source: Mercom India — DCR Module Shortage

Reason 2: Battery Storage — From Optional to Effectively Mandatory

The curtailment crisis: India’s grid is visibly struggling to absorb its own solar generation:

- 2.3 TWh of solar was curtailed between May–December 2025 due to grid security concerns (Ember Energy)

- 693 GWh was curtailed in April 2026 alone (Grid India data, via Indian Express)

- In Rajasthan — India’s largest solar state — output was cut by up to 48% during peak hours

The storage gap: China, with 1.2 TW of solar capacity, has paired it with 136 GW of new-type energy storage. India, with 150 GW of solar, has approximately 0.27 GW of installed battery storage. This comparison is not close.

The CEA projects India needs:

- 82.37 GWh of storage by 2026–27

- 411.4 GWh of storage by 2031–32

Currently, only ~13 GWh of BESS is under implementation under one VGF scheme, with another 30 GWh approved in 2025.

The policy direction: Budget 2026–27 extended customs duty exemption on capital goods for lithium-ion battery manufacturing. Budget 2025 had already exempted cobalt powder, lithium-ion battery scrap, and critical minerals. This is the government building the supply chain for a mandatory product.

When battery co-installation becomes a pre-condition for net metering approval — and the curtailment data, CEA projections, and China precedent strongly suggest it will — rooftop system costs will increase by ₹50,000–₹80,000 per installation at current battery prices.

Sources: Ember Energy | MNRE Storage Overview | Xinhua — China Storage Data

Reason 3: Structural Safety — The Unpriced Regulatory Risk

This is the factor almost no one in the rooftop solar industry is discussing publicly. And it is the one most likely to arrive suddenly.

The current ground reality: The vast majority of rooftop solar installations in India — residential, commercial, and industrial — are commissioned without any certified structural analysis. No wind load calculation per IS 875 (Part 3). No soil bearing assessment. No third-party engineering sign-off on mounting structure integrity.

Panels are being installed on RCC rooftops of unknown age, on pre-engineered building sheeting without load verification, and on structures that have never been assessed for the additional dead load and wind uplift that a solar array introduces.

Why this matters now: As rooftop panel density increases across urban and peri-urban India, the risk of panel detachment during cyclonic or high-wind events is rising. Incidents of panels dislodging during storms have already been reported across multiple states. As of now, there is no mandatory pre-installation structural certification requirement for net metering approval in most states.

What is coming: Once a significant liability event occurs — panels falling on people, structural collapse of a rooftop under solar load — regulatory response will not be gradual. DISCOMs and state electricity regulatory commissions will likely mandate a certified structural analysis report (equivalent to a STAAD Pro wind load and structural adequacy report) as a pre-condition for net metering connection approval.

This adds two costs that the market is not currently pricing:

- Direct cost: Structural engineering assessment + report — approximately ₹15,000–₹40,000 per site depending on complexity

- Time cost: Project timelines extend by 3–6 weeks minimum for assessment, redesign if required, and documentation

For commercial and industrial projects above 10 kW — where the structural stakes are higher and the regulatory scrutiny will be sharper — this will become a meaningful line item.

The industry’s current posture of ignoring this risk does not make the risk smaller. It makes the regulatory response, when it arrives, more disruptive.

Reason 4: Net Metering Rollback — The Savings Are Being Systematically Removed

What net metering gave you: A grid-tied rooftop solar system exported surplus daytime generation to the grid and received credits against nighttime consumption. For commercial and larger residential users, this “banking” of units made the ROI calculation work — often delivering payback in 4–6 years.

What is changing:

The draft 2026 amendment to the Electricity (Rights of Consumers) Rules states:

- DISCOMs may levy net metering charges for systems above 5 kW

- Time-of-day tariffs may be applied for net-billing users

The draft National Electricity Policy 2026 is more direct:

- Net metering beyond 5 kW should be “discouraged”

- Consumer storage should be promoted instead of banking

Already happening in Maharashtra: The 2025 tariff order set LT grid support charges at ₹1.96/kWh for FY 2026–27 — applicable once state rooftop capacity crosses 5,000 MW. That threshold is approaching. Systems above 10 kW in Maharashtra are already financially exposed to this charge as a near-term reality.

Who is protected, who is not:

- Sub-5 kW residential consumers: politically shielded, net metering likely to continue

- 5–500 kW systems (commercial, industrial, larger residential): being repositioned as “grid participants” — paying charges, subject to ToD pricing, savings materially reduced

The financial model that justified rooftop solar for this segment was built on free banking and generous net metering. That model is being systematically unwound — not in one sudden move, but through accumulated policy changes at central and state level.

Sources: Net Metering Amendment Rules 2021 | MAHADISCOM RRE Regulations | CEEW Rooftop Solar & Discom Revenue

The Global Warning: What Pakistan Tells Us

Pakistan’s rooftop solar boom offers the clearest available warning of what happens when cheap imported solar collides with fragile grid economics.

In 2024, Pakistan imported approximately 17 GW of Chinese solar panels. By early 2025, solar was supplying 25.3% of Pakistan’s electricity. Affluent consumers began partially exiting the grid. The cross-subsidy model — where high-tariff commercial consumers subsidize domestic and agricultural users — began to crack. The government responded by slashing buyback rates to Rs10/unit. The economics of rooftop solar deteriorated sharply for new adopters.

India’s DISCOMs are in a structurally similar position. The Ministry of Power reported that India’s distribution utilities posted a profit of ₹2,701 crore in FY 2024–25 — the first positive figure in years. But accumulated losses stand at ₹6.47 lakh crore as of 31 March 2025.

When high-paying commercial and industrial consumers reduce grid purchases through solar adoption, the cross-subsidy model erodes. Indian policymakers are acutely aware of the Pakistan precedent. The DCR mandate, net metering restrictions, and storage push are — in part — a pre-emptive response to that risk.

Sources: WEF — Pakistan Solar | Ministry of Power Annual Report 2025–26

What This Means If You Are Considering Rooftop Solar

If you are planning a residential system (1–3 kW): You are in the protected segment for now. PM Surya Ghar subsidies are still available, net metering is still generous below 5 kW, and the policy intent is to keep small homeowners shielded. The cost is rising, but this segment is least exposed to the four factors above.

If you are planning a commercial or industrial system (10 kW and above): This is where the risk is most real and most immediate. DCR cost premiums apply. Net metering savings are being reduced. Structural certification requirements are an approaching (if not yet mandatory) cost. Battery co-installation may become a condition. Every quarter you wait, the policy environment moves against your ROI.

The window that is closing: The buyers who will look back and say they timed this well are the ones installing in 2025–2026 — before battery mandates, before structural certification requirements harden, and while net metering frameworks are still relatively generous. That window is real. It is not a sales line. The policy data supports it.

Conclusion

India is not retreating from solar. It is ending the era of cheap, lightly regulated, import-dependent rooftop solar — particularly for commercial and larger users.

The emerging model is: domestically sourced panels, battery-backed systems, certified installations, and a more controlled relationship between prosumers and the grid.

Cheap solar versus sovereign solar. And right now, sovereign solar is winning.

About Lumencity: Lumencity is a Delhi-based solar lighting and rooftop solar company with government-grade installations including a 500 KW rooftop system at the Delhi Vidhan Sabha. We help residential, commercial, and institutional clients navigate India’s evolving solar landscape with honest, data-backed advice.

👉 Get a consultation: lumencity.in

All data referenced in this post is sourced from government ministries, MNRE circulars, and cited industry research. Sources linked inline throughout.